Your 5-Minute Guide to Finding the Best Travel Insurance

Answering our most commonly requested question.

Howdy—Henah here. Kayti’s heads down on her book proposal (!), so I’m sharing a topic I’ve wanted to cover ever since our launch. And it’s the one I’ve been most asked about from friends and family over the years, too: Travel insurance.

Here’s the thing: I’ve submitted claims for travel insurance that have been rejected—earlier this year, in fact. I’m no expert. But I’ve also purchased a dozen policies over the years totaling $1,000+, and successfully received more than that back from being insured, and I think it’s worth considering. And for this post, I even brought in a pro: Lauren Gumport, the VP of Communications at Faye Travel Insurance.

So without further ado, let’s get into it…

Where to find a travel insurance policy

Like all insurances, travel insurance protects your downside, should a trip go awry—and to be honest, something usually does. Baggage goes missing; flights get delayed and cause missed connections.

But there are, of course, other, bigger issues that you should get protection for: medical evacuation in case of illness, assistance with a rental car accident, or—as relevant as ever—coverage in natural disasters. And since most comprehensive policies only cost a few hundred dollars at most (when you’re spending thousands for the trip itself!), it’s the ultimate peace of mind.

For reference, Lauren shares that the most common claims submitted via Faye Travel Insurance are for: lost/delayed luggage, flight delays/cancellations, and emergency medical scenarios.

So where do you begin? IMO, there are four main buckets you can explore for finding a policy:

The first is add-on insurance during checkout when you’re booking a flight, rental, hotel, etc. I do not recommend doing this, because while it seems convenient, it’s usually too narrow a policy to be comprehensive for your entire trip. Lauren agreed: “I'd also suggest avoiding add-on insurance offerings that pop up when you're booking a hotel or flight. These are typically wrought with limitations and may only cover small aspects of your trip (such as your flight only).”

The second is your credit card travel insurance. If you have a premium card (think American Express Platinum, Chase Sapphire Reserve, Venture X), chances are there are some basic policies you may qualify for. I’ll primarily rely on these cards when I rent a car, for example, but they may offer accident assistance, lost luggage reimbursement, etc. The main caveat is that you have to book the expenses you want reimbursement for on that card in order to qualify. I don’t usually exclusively rely on credit card travel insurance, but it’s a helpful benefit.

The third is an annual policy if you travel frequently, rather than purchasing policies piecemeal for each trip. However, there are conditions to consider:

Many companies won’t cover pre-existing conditions or cancellations.

Some only keep you insured for trips up to X days.

Select annual policies have a cap on what you can claim for the entire year, so if you claim $1,000 on January 1, 2025 of your $2,000 coverage starting in January, you’ll only have $1,000 left for the remaining 364 days. Do your own due dil’ as we say on Money with Katie.

But if you travel a lot, rarely cancel, and are generally healthy, a solid annual policy for a few hundred bucks might be the way to go. Generally reputable companies include Travel Guard (Maddie’s choice), Allianz, AIG, Seven Corners, GeoBlue, and Trawick International. (Plus, you can always buy a supplemental policy for a specific trip if you need.)

Finally, you have the per trip policy. I personally prefer this route as my trips are all a little different and require slightly different coverage, and I like to compare my options on the Squaremouth platform. They compare 22 different providers (many of whom I’ve named above) along with all the separate benefits and costs, and I love their Zero Complaint Guarantee (if your claim is denied and you believe it was denied unfairly, their licensed claims adjusters will investigate and mediate your claim for you!). For reference, if you spend $2,500 on one trip for your flight and you’re in your early 30s, accommodations, and excursions, a simple comprehensive policy from one of these providers will be around $100.

Ultimately, if you have a premium travel card with strong travel insurance #bennies and your trip is fairly straightforward with lots of refundable accommodations, you may not need a separate policy—but if you prefer: coverage for more than one person, flexibility with cancellations, access to evacuation insurance or pre-existing medical coverage (which we get into below), or more comprehensive travel protection, purchasing a specific policy or annual plan is the way to go.

What should your policy include?

Now, this can’t be 100% comprehensive because everyone’s needs are a little different (you may need Extreme Sports coverage, but that will not be me 🤣), but I’ll walk you through what my bare minimum parameters are.

You’ll first be asked your age, where you’re from, where you’re heading to, your trip dates, and estimated costs. I try to keep this as accurate as possible for non-refundable costs, and Lauren agrees: “When buying a policy, you're often asked for your Total Estimated Trip Cost which should be the sum of your prepaid, non-refundable trip expenses. The higher this number, the more you'll pay for a policy. Don't over-insure yourself, meaning no need to include in this some things that you can cancel free of charge.”

I personally prefer to book travel insurance immediately after I’ve made a payment for a trip, whether that’s the flight booking or a hotel or an excursion—if there’s quite a bit of time between then and your trip, you can also usually refund your policy if you decide otherwise. Typically, you’ll want to book travel insurance no more than 14 days after your first payment or booking.

For my procrastinators, Lauren mentions, “If you want to buy travel insurance last-minute, you can usually do so at a lower cost,” but you won’t be “eligible for trip cancellation benefits if buying a policy within 48 hours of your departure date.” (This varies, as some policies often go into effect the next day, but again, do your own due dil’.)

Here are the filters I check for on Squaremouth:

Emergency Medical: For unexpected illness/injury while traveling, if you need a hospital or doctor. This is a non-negotiable for me and I’ll usually look for a minimum of $250,000–$500,000 in primary medical coverage (i.e., it’ll kick in before any sort of US-based policy).

Medical Evacuation: Another non-negotiable, in case you need to be transported to a medical facility elsewhere or even flown back home. I have a friend who was evacuated from Singapore after coming down with typhoid, so this is not the part of the policy you want to skimp on! I usually look for $500,000–$1,000,000 in medical evacuation coverage.

Trip Interruption: Coverage if you need to return home early or miss a portion of your trip—it provides reimbursement for unused trip costs and transportation expenses to come home. Having trip interruption is usually standard in a policy so I like to include this filter no matter what, since life happens.

Travel Delay: This is another usual part of a policy, as it’ll help reimburse for meals, accommodations, and transportations if you’re delayed on a common carrier. When we were stranded in Santorini because our ferry to Naxos could not operate under the inclement weather (lol, see photo below), our Travel Delay benefits were extremely helpful here, in addition to the Trip Interruption and Hurricane and Weather benefits.

Baggage Delay / Loss: Again, this is pretty standard, but the amount you’ll receive might vary usually up to $500 per person per day. (But if you’re #TeamCarryOn, this may not even be an issue for you. 😉)

Cancel for Any Reason (CFAR): In recent years, I’ve started to pay for this benefit. The pandemic, last-minute health issues, layoffs or moving, family problems, even just chickening out on solo travel (guilty); there might always be a reason you need to cancel. If you’ve invested a ton of money into your trip, adding a CFAR benefit will increase your policy by 40–60%, but it will also give you security that you’ll be covered no matter the reason you decide not to go. You may only get 75% back of your costs, but it’s better than $0. So for example, if you’re spending $4,000 on a trip and a CFAR policy is $200, you’d spend $200 to ultimately get $3,000 back—and that’s a worthwhile gamble to me.

Pre-existing Medical: If you have a chronic condition you want coverage for on the trip, you’ll need to add this to your policy and it’s only available up to 14–30 days from your trip deposit or before you make a final payment. This varies widely, so check the fine print.

Hurricane & Weather: This has become an increasingly important filter to include, given *gestures around* the realities of climate change. If you’re traveling somewhere where weather may impact your trip severely, it’s always worth adding on. Most important note here: You won’t receive coverage for this if you purchase a policy after a storm has already been named.

The TL;DR: Always err on the side of caution for medical expenses, delays, and weather issues, and book early for the most comprehensive coverage.

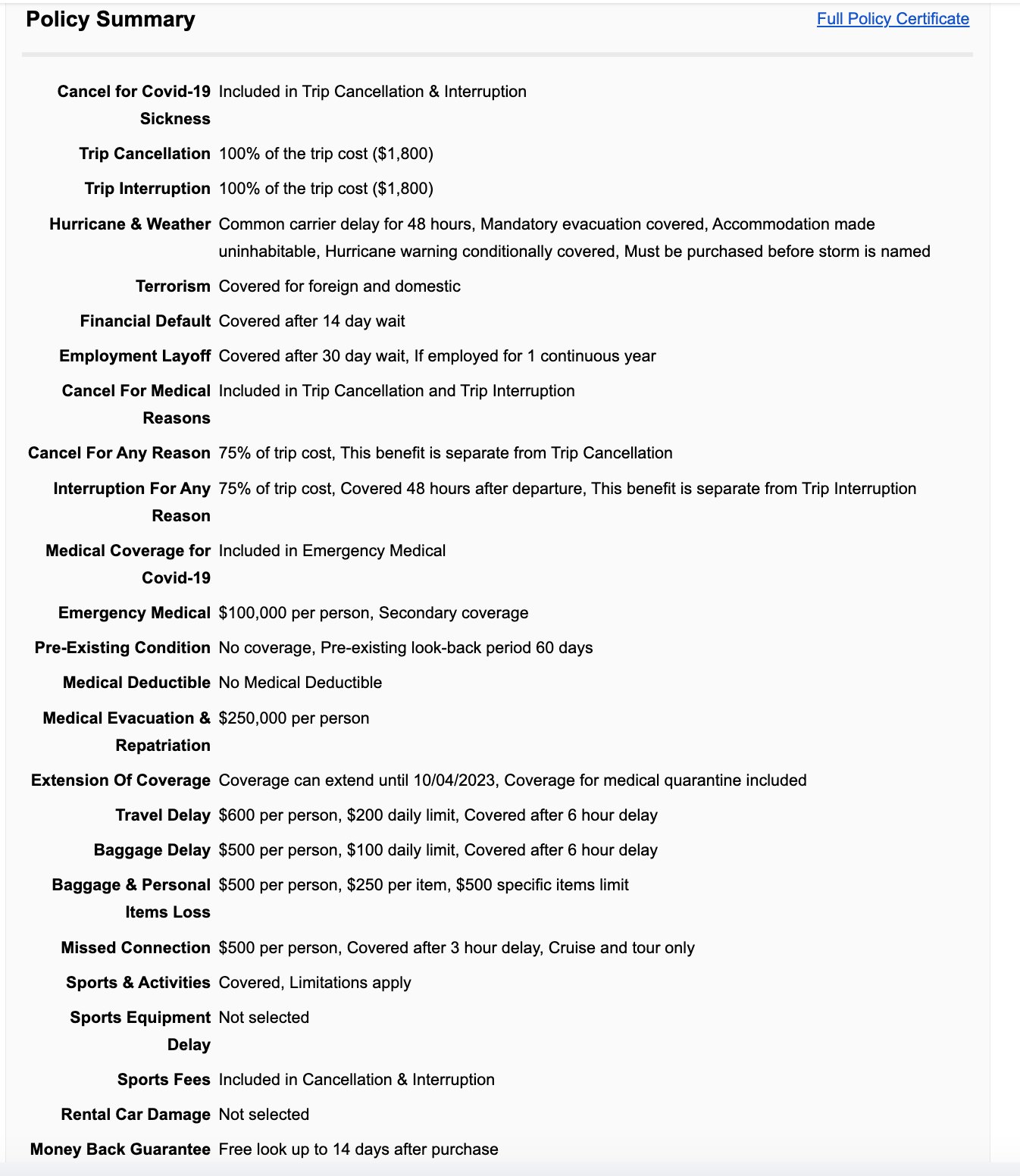

Here’s an example of a policy I purchased through Squaremouth this past year—I spent ~$2,500 in non-refundable costs on a six-day trip to Mexico, and I paid $79.75 for this coverage:

This final tip here is probably overkill, but if you’re a Spreadsheet Girly like me, you might enjoy it: When I’m not sure which policy is best, I’ll make a Google Sheet and compare both the costs and benefits. Some businesses offer multiple policies with slight variants/cost differences, too (like Travel Guard Essential vs. Preferred below), so this helps me see them all at a high level.

Here’s an example from our trip earlier this year to Italy:

So those are the quick ‘n dirty basics—and a few last tips:

I asked Lauren what the most common mistakes travelers make when submitting a claim, and she said, “Not uploading all of their documentation, and then forgetting to do so. And in certain scenarios, you may need documents for airlines.”

Needing airline documentation has happened to me on more than one occasion, so make sure you have this handy if you need it (and try to take screenshots in the moment when you get alerts)! Keep proof of receipts and all documentation, and essentially over-document—Maddie, my friend and previously featured travel agent, echoes this advice as well.

Finally, Lauren noted, “With missing luggage, the best thing you can do when claiming with your insurance or with the airline is get a PIR (property irregularity report) from the airline. You should do this when you're at baggage claim and before you leave the airport.”

I’m pretty sure Substack’s going to cut me off soon, so perhaps more on knowing how to file a claim will be another post—what do we think? Maybe to expand on why certain claims were rejected? Yay/nay?

And if you have any other questions on finding the best travel insurance, ask away!

🌴 CN Traveler revealed their 2024 Readers Choice Awards. While I can’t afford most of these picks 😂, they do leave me inspired. I mean… #11 in Marrakech?

💳 Now’s the time to get ahead on sign-up bonuses for end-of-year spending. Here are the best credit card offers for October!

👀 If you’re booking hotels soon and have the AmEx Platinum, I’m seeing a ton of cash-back deals, including $100 back on $500+ spent on Preferred Hotels and Resorts. If you don’t yet have this card, check it out here (*referral)—I find it pays itself off quickly and their customer service is excellent.

🎧 I recently gifted this to my husband to use on upcoming flights, and he said it worked really well on our trip home last weekend.

🤫 Loving this piece from

on romanticizing a quiet life; it really speaks to the power of solo travel and solitude: “Solitude is when everything around me falls silent. It’s magical—a soundless apocalypse in the way the world suddenly reduces to nothing but myself.”

Stay safe and healthy—and see y’all next week!

—Henah

🙃 weekend mood brought to you this week from when I was stranded in oía, santorini, thanks to a mediterranean hurricane:

Thank you for this very helpful post! I’ve always gotten travel insurance but find it confusing. If a hotel reservation is refundable if you cancel at least 48 or 72 hours in advance, should you not include that in the trip cost since it’s refundable? Or should you include it since it’s only refundable up to a certain point? I’ve never been sure about what to include in that total trip cost.